dear W :

many thanks...i shall attempt to find some useful FA at your suggested threads...

|

|

|

Hyflux

Re: Hyflux

![]() by kennynah » Wed Jul 09, 2008 12:03 pm

by kennynah » Wed Jul 09, 2008 12:03 pm

Options Strategies & Discussions  .(Trading Discipline : The Science of Constantly Acting on Knowledge Consistently - kennynah).Investment Strategies & Ideas

.(Trading Discipline : The Science of Constantly Acting on Knowledge Consistently - kennynah).Investment Strategies & Ideas

..................................................................<A fool gives full vent to his anger, but a wise man keeps himself under control-Proverbs 29:11>.................................................................

..................................................................<A fool gives full vent to his anger, but a wise man keeps himself under control-Proverbs 29:11>.................................................................

.(Trading Discipline : The Science of Constantly Acting on Knowledge Consistently - kennynah).Investment Strategies & Ideas-

kennynah - Lord of the Lew Lian

- Posts: 16005

- Joined: Wed May 07, 2008 2:00 am

- Location: everywhere.. and nowhere..

Re: Hyflux

![]() by 8percentpa » Tue Jul 15, 2008 12:27 pm

by 8percentpa » Tue Jul 15, 2008 12:27 pm

Hyflux is already damn bloody expensive where it is trading today.

Its revenue is a mere 180mn but its mkt cap is 1bn.

For normal co usually the mkt cap is equal to its revenue.

For the stock to be trading at $10 ie 4-5bn, its revenue has to grow 25x to 4-5bn.

That is why it will not trade at $10, unless the market goes wild and buy Hyflux without considering its fundamentals.

Why is Hyflux revenue so weak remains a mystery to me.

I suspect it has very little so-called core earnings (sustainable earnings after the construction is done)

So this means that it has to continuously win bids and built plants.

This is then a fundamentally very weak business model bcos how many plants can you build?

The world already has 13,000 desalination plants.

And competition will catch up.

Also Hyflux doesnt really own the membrane technology.

They just buy from some Japanese co.

If I were Olivia Lum, I will find some private banker and structure a deal to cash out at today's share price! Hehe.

Its revenue is a mere 180mn but its mkt cap is 1bn.

For normal co usually the mkt cap is equal to its revenue.

For the stock to be trading at $10 ie 4-5bn, its revenue has to grow 25x to 4-5bn.

That is why it will not trade at $10, unless the market goes wild and buy Hyflux without considering its fundamentals.

Why is Hyflux revenue so weak remains a mystery to me.

I suspect it has very little so-called core earnings (sustainable earnings after the construction is done)

So this means that it has to continuously win bids and built plants.

This is then a fundamentally very weak business model bcos how many plants can you build?

The world already has 13,000 desalination plants.

And competition will catch up.

Also Hyflux doesnt really own the membrane technology.

They just buy from some Japanese co.

If I were Olivia Lum, I will find some private banker and structure a deal to cash out at today's share price! Hehe.

I belong to a group of investors believing in obscure stuff like value-for-money, contrarian thinking, mean reversion etc. My blog at

http://8percentpa.blogspot.com

http://8percentpa.blogspot.com

- 8percentpa

- Loafer

- Posts: 8

- Joined: Tue May 20, 2008 9:06 am

Re: Hyflux

![]() by kennynah » Tue Jul 15, 2008 1:59 pm

by kennynah » Tue Jul 15, 2008 1:59 pm

8percentpa wrote:If I were Olivia Lum, I will find some private banker and structure a deal to cash out at today's share price! Hehe.

that's a nice perspective...

as for the above...i venture a guess ...what would she do if hyflux is "taken" away from her? have we not noticed that there are countless CEOs running shops here just for the monthly paycheques?

Options Strategies & Discussions .(Trading Discipline : The Science of Constantly Acting on Knowledge Consistently - kennynah).Investment Strategies & Ideas

..................................................................<A fool gives full vent to his anger, but a wise man keeps himself under control-Proverbs 29:11>.................................................................

.(Trading Discipline : The Science of Constantly Acting on Knowledge Consistently - kennynah).Investment Strategies & Ideas-

kennynah - Lord of the Lew Lian

- Posts: 16005

- Joined: Wed May 07, 2008 2:00 am

- Location: everywhere.. and nowhere..

Re: Hyflux

![]() by tangoandrew » Tue Jul 15, 2008 2:23 pm

by tangoandrew » Tue Jul 15, 2008 2:23 pm

have we not noticed that there are countless CEOs running shops here just for the monthly paycheques?

towkay K....gotta agree with you...and it is the [blur] retail investors who are the ones sponsoring them to enjoy this privilege and other bonuses.

- tangoandrew

- Loafer

- Posts: 21

- Joined: Fri Jun 20, 2008 11:46 pm

Re: Hyflux

![]() by kennynah » Tue Jul 15, 2008 2:26 pm

by kennynah » Tue Jul 15, 2008 2:26 pm

hi tangoandrew..

i was one of those goondus..buy this company shares and for years, nothing ever happens to this company except share price keeps dropping...but just somehow, company wont collapse nor delisted...every time i see their yearly financial statements, knn...so much money goes to the ceo's pocket...

then, your words above reminded me of how i felt... gong gong...hahaha

i was one of those goondus..buy this company shares and for years, nothing ever happens to this company except share price keeps dropping...but just somehow, company wont collapse nor delisted...every time i see their yearly financial statements, knn...so much money goes to the ceo's pocket...

then, your words above reminded me of how i felt... gong gong...hahaha

Options Strategies & Discussions .(Trading Discipline : The Science of Constantly Acting on Knowledge Consistently - kennynah).Investment Strategies & Ideas

..................................................................<A fool gives full vent to his anger, but a wise man keeps himself under control-Proverbs 29:11>.................................................................

.(Trading Discipline : The Science of Constantly Acting on Knowledge Consistently - kennynah).Investment Strategies & Ideas-

kennynah - Lord of the Lew Lian

- Posts: 16005

- Joined: Wed May 07, 2008 2:00 am

- Location: everywhere.. and nowhere..

Re: Hyflux

![]() by tangoandrew » Tue Jul 15, 2008 2:37 pm

by tangoandrew » Tue Jul 15, 2008 2:37 pm

cannot blame yourself bec of the power spin & support given to the co that inflated its potential, etc...

even when i wasn't following the mkt, i was aware of the co...thru the TV news propaganda.

when i started tracking the mkt last sept....i couldn't understand why it didn't fly despite the fact that it is into water-related biz.

even when i wasn't following the mkt, i was aware of the co...thru the TV news propaganda.

when i started tracking the mkt last sept....i couldn't understand why it didn't fly despite the fact that it is into water-related biz.

- tangoandrew

- Loafer

- Posts: 21

- Joined: Fri Jun 20, 2008 11:46 pm

Re: Hyflux

![]() by chaibu » Tue Jul 15, 2008 2:38 pm

by chaibu » Tue Jul 15, 2008 2:38 pm

Towkay,

You are spot on!

By and large CEOs are working for themselves.

Their stories are like.....everywhere...and nowhere

You are spot on!

By and large CEOs are working for themselves.

Their stories are like.....everywhere...and nowhere

- chaibu

- Loafer

- Posts: 42

- Joined: Wed Jul 09, 2008 12:13 pm

Re: Hyflux

![]() by kennynah » Tue Jul 15, 2008 2:39 pm

by kennynah » Tue Jul 15, 2008 2:39 pm

chaibu wrote:...Their stories are like.....everywhere...and nowhere

chaibu:

Options Strategies & Discussions .(Trading Discipline : The Science of Constantly Acting on Knowledge Consistently - kennynah).Investment Strategies & Ideas

..................................................................<A fool gives full vent to his anger, but a wise man keeps himself under control-Proverbs 29:11>.................................................................

.(Trading Discipline : The Science of Constantly Acting on Knowledge Consistently - kennynah).Investment Strategies & Ideas-

kennynah - Lord of the Lew Lian

- Posts: 16005

- Joined: Wed May 07, 2008 2:00 am

- Location: everywhere.. and nowhere..

Re: Hyflux

![]() by iam802 » Tue Aug 05, 2008 4:27 pm

by iam802 » Tue Aug 05, 2008 4:27 pm

Hyflux..sell off?

1. Always wait for the setup. NO SETUP; NO TRADE

2. The trend will END but I don't know WHEN.

TA and Options stuffs on InvestIdeas:

The Ichimoku Thread | Option Strategies Thread | Japanese Candlesticks Thread

2. The trend will END but I don't know WHEN.

TA and Options stuffs on InvestIdeas:

The Ichimoku Thread | Option Strategies Thread | Japanese Candlesticks Thread

-

iam802 - Big Boss

- Posts: 6352

- Joined: Wed May 07, 2008 1:14 am

Re: Hyflux

![]() by iam802 » Wed Aug 06, 2008 7:05 pm

by iam802 » Wed Aug 06, 2008 7:05 pm

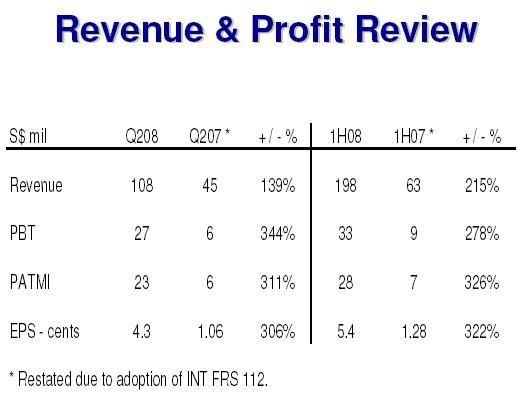

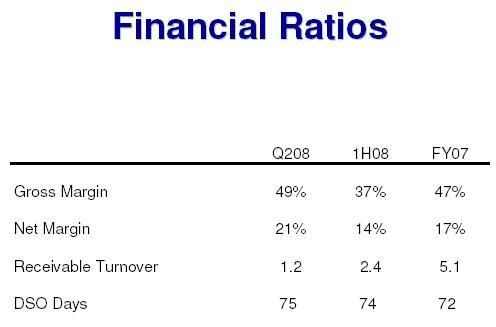

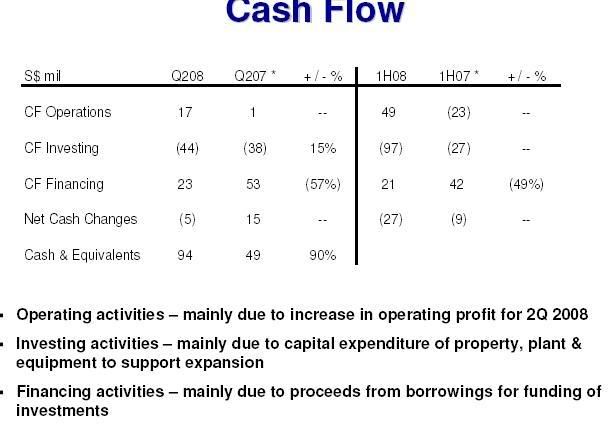

Thanks to San for sharing this info.

Pretty good results... but sentiments still seems weak (after I look at the chart in the morning).

http://info.sgx.com/webcoranncatth.nsf/ ... penelement

---

results screen shot

Pretty good results... but sentiments still seems weak (after I look at the chart in the morning).

http://info.sgx.com/webcoranncatth.nsf/ ... penelement

---

results screen shot

1. Always wait for the setup. NO SETUP; NO TRADE

2. The trend will END but I don't know WHEN.

TA and Options stuffs on InvestIdeas:

The Ichimoku Thread | Option Strategies Thread | Japanese Candlesticks Thread

2. The trend will END but I don't know WHEN.

TA and Options stuffs on InvestIdeas:

The Ichimoku Thread | Option Strategies Thread | Japanese Candlesticks Thread

-

iam802 - Big Boss

- Posts: 6352

- Joined: Wed May 07, 2008 1:14 am

Who is online

Users browsing this forum: No registered users and 1 guest